Dealing with Aggressive Banks

Dealing with Aggressive Banks

This post on dealing with aggressive banks is a follow on to my previous post on ‘Why Banks are Closing Overdraft Accounts‘ – which has been alarmingly popular because it is such a common ‘tool’ of the Irish banking system in 2012. It is very popular in order to facilitate banks fiddling with the optics of their ‘lending books’ which are, to all intents and purposes, totally closed. The banks are committed to give out a certain amount of ‘new lending’ in order to qualify for Irish taxpayer funded bailouts but a loophole left in the terms allows them to simply ‘reassign’ accounts rather than doing any actual lending – and the banks have, as is their wont, gleefully bounded into the loophole. Do please read the article, even if I say so myself it is a lesson on just how devious the banking industry can be and the level of hubris that remains, despite the fact that the Irish banks are largely responsible for bringing Ireland to its knees financially, where it currently resides.

In any case, this post is not here to go back over that ground, it is instead meant to give some guidance to those who are dealing with aggressive banks – and there are a lot of people in this situation. You are not alone, but this fact in itself will be of no solace at all to people who are dealing with aggressive banks at this point in time.

You may ask why I’m broaching this subject at all and it is a good question. I’ve been contacted by quite a few people about dealing with aggressive banks because those with loans taken out to fund property purchases overseas tend to be very high on banks’ hit-list when it comes to getting aggressive about receiving repayment.

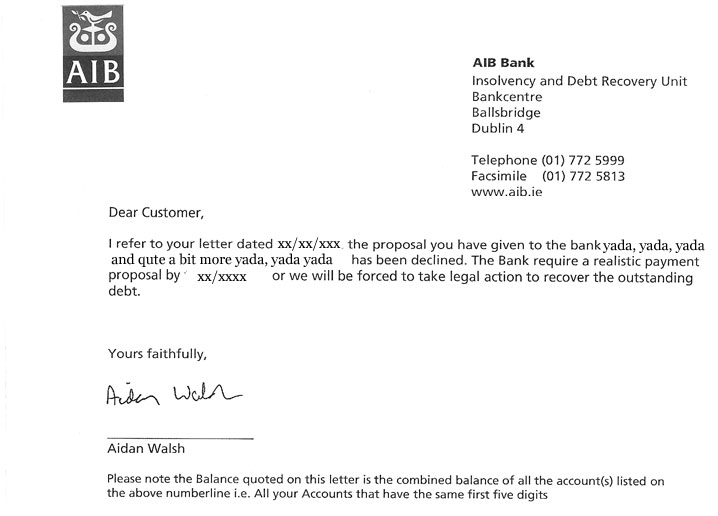

If you have been dealing with aggressive banks, particularly AIB, then you’ll most likely have been in receipt of a letter such as the one below from Aidan Walsh in AIB (significantly edited to protect the anonymity of the unfortunate recipient) or his peers in Bank of Ireland, Permanent TSB, or wherever.

They’re of a muchness really – it’s as if they all meet up regularly in the CityWest Hotel for a briefing on how best to bully their clients (which ironically own AIB and a big chunk of BoI). We all know where incessant bank bullying has led in recent times – it is not pretty nor is it morally acceptable – but this worries the banks not one bit as nobody is ever made legally responsible by being taken through the courts. We can’t even bring a case against those at the top of the banking pyramid when they bring our economy tumbling down around us so minions further down the ladder can act safely in the knowledge that they will never face legal consequences for their actions.

The first thing to note here is that we’ve noticed a very alarming trend when dealing with aggressive banks. There are an awful lot of banks with incomplete documentation, particularly relating to security for loans taken out, but also relating to what the loan is for, when full repayment is due and how exactly that full repayment should be facilitated. Security is the item on which the bank has lent money and on which it normally wishes to have ‘first call’ should the borrower default on his or her repayments. It appears that banks have trawled through their loan books (they may as well, they’re doing pretty much nothing else at the moment) and have found huge black holes in their security and the documentation filled out in order to secure assets for loan purposes. This is a result of the slipshod manner in which they grabbed everything they could get their hands on during the boom of the mid-noughties. The birds are coming home to roost on this issue at the moment.

So you might well think that the banks would gently approach their customers to point out the irregularity in their documentation and to have matters sorted amicably. You’d be entirely wrong. Such is the level of arrogance in these bloated and outdated institutions that the first port of call is full on attack. In fact, we’ve noticed, the more trouble the bank is in regarding a loan the more aggressively it approaches the matter.

Irish Banks to Sell on their Loan Books

It is also being very heavily intimated that the banks are currently ‘cleaning up their loan books’ in order to sell them on – most likely at around 4oc in the Euro. This has made them even more aggressive but it also opens the potential for negotiation. This will only be the case if you know their weak spots to facilitate this negotiation. If documentation is not in order you have the bank over a barrel, but you need to know how to turn the screw. It should also be noted that bad and all as Irish banks are, they’re probably a lot easier to deal with than the ‘loan sharks’ to which they are likely to sell their loan books. They are, at least to some extent, governed by the rules and regulations set down by the Irish government when bailing them out of the awful mess into which they got themselves.

Dealing With Aggressive Banks – What Should I Do?

This is all well and good for the borrower dealing with aggressive banks, but how do you take advantage of the predicament in which banks have put themselves? The answer is that it is virtually impossible to do it on your own unless you have knowledge of how the banking system works at the top end – and most people obviously don’t. Otherwise this informaiton is really of no advantage to you at all. You need to know what steps the bank is looking to take and what steps you can take to mitigate any steps they are likely to take in advance. Unfortunately you need an expert in this particular market sector to take the bank on at their own game.

Luckily, from my dealings in the market over a long period of years I have access to experts who are adept at dealing with aggressive banks. The bad news is that these experts don’t work for nothing – such is capitalism I’m afraid.

If, however, you believe you are dealing with aggressive banks, particular one you feel is being overly aggressive with a specific account, and you are in a position to pay somebody to deal with this bank on your behalf, you could well find that the result will be very well worth the investment.

Feel free to drop me a line on info@diarmaidcondon.com if you think this service may one from which you could benefit.

I am a victim of the Landsbanki Luxembourg “Equity Release Scam” and came to your site after researching ME and in particular Santiago De La Cruz. He has received enormous fee income for representing 180 victims and delivered very little over the last 5 years.See http://www.landsbankivictims.co.uk for a detailed account to date.I am considering any viable alternative to bring matters to a speedy conclusion but if SDLC is to be believed this may be problematical in Spain.

Any useful input would be appreciated,Roger Fish